Retirement savings are critical role for ensuring financial security of employees in the post-retirement phase, and a variety of factors significantly influence employees` ability to make retirement savings. The existence of retirement savings is important when planning for retirement mainly in the face of increased life expectancy, high cost of living, and the increased retirement age of employees in Zimbabwe. This research sought to examine the determining factors of retirement savings among employees in tertiary institutions with focus on one institution in Harare. The determinants that affect workers` retirement savings are identical across all other tertiary institutions hence the findings from the study would be a representative of other tertiary institutions across Zimbabwe. The study adopted a positivist paradigm and was a case study research where a sample of sixty respondents out of an accessible population of six-hundred staff establishment. The population was stratified into lecturing and non-lecturing staff. Simple random sampling was employed to come up with a sample size of sixty (60) respondents. Structured questionnaires and interview guides were used for collection of data. The study established that retirement savings were affected by age, marital status, gender, family size, family expenditure, level of education, financial literacy levels, interest rate, income level, exchange rate, and inflation rate. The study recommended that employees should attend financial literacy trainings together with savings and investment conferences so as to acquaint themselves with the general savings and investment management process that they could use. Such trainings would expose employees to various financial products such as shares, term deposits, unit trusts, cash savings, gold coins, investment in livestock, properties, diversified asset portfolio, fixed savings accounts, income generating projects, and other small business entrepreneurial ventures and start-ups. The management of tertiary institutions were recommended to positively influence employees to engage in retirement savings by funding employees to attend financial literacy and investment management training such that they would acquire the necessary knowledge to make savings and investments for post-retirement. Furthermore, institutions were recommended to hold quarterly and semi-annual seminars and conferences on retirement planning and retirement savings and make attendance by employees’ mandatory such that their attitude on retirement savings increases.

| Published in | Science Futures (Volume 1, Issue 1) |

| DOI | 10.11648/j.scif.20250101.13 |

| Page(s) | 21-27 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Retirement, Savings, Socio-demographic, Economic, Investment, Financial Literacy

NSSA | National Social Security Authority |

ZIMSTATS | Zimbabwe Statistical Agency |

USD | United States Dollar |

ZWD | Zimbabwean Dollar |

SSA | Sub Saharan Africa |

HIV | Human Immune Virus |

AIDS | Acquired Immune Deficiency Syndrome |

AFD | African Development Bank |

| [1] | Abidin, Z. Z., & Zainuddin, A. (2021). Financial Literacy on Retirement Planning Among Working Single Women In Private Sector, Selangor. The 2nd International Conference on Innovations in Social Sciences Education and Engineering ( ICoISSEE ), 1-15. |

| [2] | African Development Bank Group. (2024). Country Focus Report 2024. African Development Bank Group. |

| [3] | Blessing, O., & Ph, A. N. D. (2021). Retirement Planning Involvement and Challenges Encountered by Staff of Public Universities in Rivers State, Nigeria. 4002(4), 243-251. |

| [4] | Boddy, D., Dokko, J., Hershbein, B., & Kearney, M. S. (2015). Ten Economic Facts about Financial Well-Being in Retirement. |

| [5] | Comerton-Forde, C., de New, J., Salamanca, N., Ribar, D. C., Nicastro, A., & Ross, J. (2022). Measuring Financial Wellbeing with Self-Reported and Bank Record Data*. Economic Record, 98(321), 133-151. |

| [6] | Dhlembeu, N. T., Kekana, K., & Mvita, M. F. (2023). The Influence of Financial Literacy on Retirement Planning in South Africa. In SSRN Electronic Journal. |

| [7] | Embong, A. M., Afzainizam, N., Norhashim, M., & Ahmadi, A. (2021). Investigating the business performance on the financial well-being of the Government retirees. SHS Web of Conferences, 124, 03006. |

| [8] | Fanta, A., & Mutsonziwa, K. (2021). Financial Literacy as a Driver of Financial Inclusion in Kenya and Tanzania. |

| [9] | Ghadwan, A., Marhaini, W., Ahmad, W., & Hanifa, M. H. (2022). Financial Planning for Retirement : The Mediating Role of Culture. |

| [10] | Ghadwan, A. S., Wan Ahmad, W. M., & Hisham Hanifa, M. (2023). Financial Planning for Retirement: The Moderating Role of Government Policy. SAGE Open, 13(2), 1-16. |

| [11] | Hassan, K. H., Rahim, R. A., Ahmad, F., Tengku Zainuddin, T. N. A., Merican, R. R., & Bahari, S. K. (2016). Retirement Planning Behaviour of Working Individuals and Legal Proposition for New Pension System in Malaysia. Journal of Politics and Law, 9(4), 43. |

| [12] | Hauff, J. C., Carlander, A., Gärling, T., & Nicolini, G. (2020). Retirement Financial Behaviour: How Important Is Being Financially Literate? Journal of Consumer Policy, 43(3), 543-564. |

| [13] | Jaffar, N., Mohd Faizal, S., Selamat, Z., Awaludin, I. S., & Sulaiman, N. A. (2024). Financial literacy and financial well-being of low-income women in Malaysia: a capability view. Cogent Social Sciences, 10(1). |

| [14] | Kamakia, M. G., Mwangi, C. I., & Mwangi, M. (2017). Financial Literacy and Financial Wellbeing of Public Sector Employees: A Critical Literature Review. European Scientific Journal, ESJ, 13(16), 233. |

| [15] | Karakara, A. A.-W., Sebu, J., & Dasmani, I. (2022). Financial literacy, financial distress and socioeconomic characteristics of individuals in Ghana. African Journal of Economic and Management Studies, 13(1), 29-48. |

| [16] | Khawar, S., & Sarwar, A. (2021). Financial literacy and financial behavior with the mediating effect of family financial socialization in the financial institutions of Lahore, Pakistan. Future Business Journal, 7(1), 1-11. |

| [17] | Kim, K. T., & Lee, J. (2024). Unlocking Financial Well-Being for People With Disabilities: The Importance of Financial Knowledge and Socialization Within the Family Context. SAGE Open, 14(2). |

| [18] | Mohd, J., Kadir, A., Zainon, S., Fadhilah, R., Noor, S., & Aziz, A. (2020). Retirement Planning and its Impact on Working Individuals. 7(06), 1550-1559. |

| [19] | Mokhtar, N., & Husniyah, A. R. (2017). Social sciences & humanities Determinants of Financial Well-Being among Public Employees in Putrajaya, Malaysia. Pertanika J. Soc. Sci. & Hum, 25(3), 1241-1260. |

| [20] | Mustafa, W. M. W., Islam, M. A., Asyraf, M., Hassan, M. S., Royhan, P., & Rahman, S. (2023). The Effects of Financial Attitudes, Financial Literacy and Health Literacy on Sustainable Financial Retirement Planning: The Moderating Role of the Financial Advisor. Sustainability (Switzerland), 15(3). |

| [21] | Ncube, C. M., & Goodman Nhapi, T. (2022). Un-African Aging? Discourses of the Socio-Spatial Welfare for Older People in Urban Zimbabwe. Architecture and Culture, 10(1), 156-173. |

| [22] | Njoka, C. (2021). Financial literacy and personal retirement planning : a socioeconomic approach. 1(2), 121-134. |

| [23] | Olubukola, O. A., Kudzanai, M., Shepard, M., Thomas, B., & Obert, S. (2021). Saving practices and economic performance: A Zimbabwean case 1980-2015. In Asian Economic and Financial Review (Vol. 11, Issue 2, pp. 118-128). Asian Economic and Social Society. |

| [24] | Rubaba, L. (2015). Savings Culture in Zimbabwe Post Dollarization: Policy Issues. |

| [25] | Sajuyigbe, A. S., Adegun, E. A., Adeyemi, F., Johnson, A. A., Oladapo, J. T., & Jooda, D. T. (2024). The Interplay of Financial Literacy on the Financial Behavior and Well-being of Young Adults: Evidence from Nigeria. Jurnal Ilmu Ekonomi Terapan, 9(1), 120-136. |

| [26] | Saunders, M., Lewis, P., & Thornhill, A. (2007). Research Methods for Buniess Students. In Pearson. |

| [27] | So, W. K. W., Au, D. W. H., Chan, D. N. S., Ng, M. S. N., Choi, K. C., Xing, W., Chan, M., Mak, S. S. S., Ho, P. S., Tong, M., Au, C., Ling, W. M., Chan, M., & Chan, R. J. (2023). Financial well-being as a mediator of the relationship between multimorbidity and health-related quality of life in people with cancer. Cancer Medicine, 12(14), 15579-15587. |

| [28] | Soepding, B. A., Munene, J. C., & Dang, D. Y. (2022). Financial well-being of Retirees Community in Nigeria. In Journal of Enterprising Communities (Vol. 16, Issue 2, pp. 341-358). |

| [29] | Surya Dewi, P. S., Margaretha Leon, F., & Endang Purba, Y. (2023). Factors that affect financial well-being in master program students. International Journal of Management Studies and Social Science Research, 05(01), 163-174. |

| [30] |

Tafirenyika, N., & Kuye, J. O. (2016). The social security policy of the Government of Zimbabwe: a policy analysis overview.

http://upetd.up.ac.za/authors/create/plagiarism/students.htm |

| [31] | Theodorus Sutadi, & Tri Rahmawati, C. H. (2024). The Influence of Financial Literacy on Green Investment Decisions. Al-Kharaj: Jurnal Ekonomi, Keuangan & Bisnis Syariah, 6(6). |

| [32] | Yahiaoui, N. E. H. (2023). Demographic and socio-economic determinants of multidimensional financial literacy among young algerian university students. Journal of Management and Business Education, 6(2), 199-221. |

| [33] | Zazili, A. S. A., Ghazali, M. F. Bin, Abu Bakar, N. T. B., Ayob, M. B., & Samad, I. H. B. A. (2017). Retirement Planning: Young Professionals in Private Sector. SHS Web of Conferences, 00024. |

APA Style

Dhewa, C., Makurumidze, S., Mashizha, M. (2025). Determinants for Retirement Savings of Employees in Tertiary Institutions of Zimbabwe. Science Futures, 1(1), 21-27. https://doi.org/10.11648/j.scif.20250101.13

ACS Style

Dhewa, C.; Makurumidze, S.; Mashizha, M. Determinants for Retirement Savings of Employees in Tertiary Institutions of Zimbabwe. Sci. Futures 2025, 1(1), 21-27. doi: 10.11648/j.scif.20250101.13

AMA Style

Dhewa C, Makurumidze S, Mashizha M. Determinants for Retirement Savings of Employees in Tertiary Institutions of Zimbabwe. Sci Futures. 2025;1(1):21-27. doi: 10.11648/j.scif.20250101.13

@article{10.11648/j.scif.20250101.13,

author = {Clever Dhewa and Shepard Makurumidze and Margaret Mashizha},

title = {Determinants for Retirement Savings of Employees in Tertiary Institutions of Zimbabwe},

journal = {Science Futures},

volume = {1},

number = {1},

pages = {21-27},

doi = {10.11648/j.scif.20250101.13},

url = {https://doi.org/10.11648/j.scif.20250101.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.scif.20250101.13},

abstract = {Retirement savings are critical role for ensuring financial security of employees in the post-retirement phase, and a variety of factors significantly influence employees` ability to make retirement savings. The existence of retirement savings is important when planning for retirement mainly in the face of increased life expectancy, high cost of living, and the increased retirement age of employees in Zimbabwe. This research sought to examine the determining factors of retirement savings among employees in tertiary institutions with focus on one institution in Harare. The determinants that affect workers` retirement savings are identical across all other tertiary institutions hence the findings from the study would be a representative of other tertiary institutions across Zimbabwe. The study adopted a positivist paradigm and was a case study research where a sample of sixty respondents out of an accessible population of six-hundred staff establishment. The population was stratified into lecturing and non-lecturing staff. Simple random sampling was employed to come up with a sample size of sixty (60) respondents. Structured questionnaires and interview guides were used for collection of data. The study established that retirement savings were affected by age, marital status, gender, family size, family expenditure, level of education, financial literacy levels, interest rate, income level, exchange rate, and inflation rate. The study recommended that employees should attend financial literacy trainings together with savings and investment conferences so as to acquaint themselves with the general savings and investment management process that they could use. Such trainings would expose employees to various financial products such as shares, term deposits, unit trusts, cash savings, gold coins, investment in livestock, properties, diversified asset portfolio, fixed savings accounts, income generating projects, and other small business entrepreneurial ventures and start-ups. The management of tertiary institutions were recommended to positively influence employees to engage in retirement savings by funding employees to attend financial literacy and investment management training such that they would acquire the necessary knowledge to make savings and investments for post-retirement. Furthermore, institutions were recommended to hold quarterly and semi-annual seminars and conferences on retirement planning and retirement savings and make attendance by employees’ mandatory such that their attitude on retirement savings increases.},

year = {2025}

}

TY - JOUR T1 - Determinants for Retirement Savings of Employees in Tertiary Institutions of Zimbabwe AU - Clever Dhewa AU - Shepard Makurumidze AU - Margaret Mashizha Y1 - 2025/12/09 PY - 2025 N1 - https://doi.org/10.11648/j.scif.20250101.13 DO - 10.11648/j.scif.20250101.13 T2 - Science Futures JF - Science Futures JO - Science Futures SP - 21 EP - 27 PB - Science Publishing Group SN - 3070-6289 UR - https://doi.org/10.11648/j.scif.20250101.13 AB - Retirement savings are critical role for ensuring financial security of employees in the post-retirement phase, and a variety of factors significantly influence employees` ability to make retirement savings. The existence of retirement savings is important when planning for retirement mainly in the face of increased life expectancy, high cost of living, and the increased retirement age of employees in Zimbabwe. This research sought to examine the determining factors of retirement savings among employees in tertiary institutions with focus on one institution in Harare. The determinants that affect workers` retirement savings are identical across all other tertiary institutions hence the findings from the study would be a representative of other tertiary institutions across Zimbabwe. The study adopted a positivist paradigm and was a case study research where a sample of sixty respondents out of an accessible population of six-hundred staff establishment. The population was stratified into lecturing and non-lecturing staff. Simple random sampling was employed to come up with a sample size of sixty (60) respondents. Structured questionnaires and interview guides were used for collection of data. The study established that retirement savings were affected by age, marital status, gender, family size, family expenditure, level of education, financial literacy levels, interest rate, income level, exchange rate, and inflation rate. The study recommended that employees should attend financial literacy trainings together with savings and investment conferences so as to acquaint themselves with the general savings and investment management process that they could use. Such trainings would expose employees to various financial products such as shares, term deposits, unit trusts, cash savings, gold coins, investment in livestock, properties, diversified asset portfolio, fixed savings accounts, income generating projects, and other small business entrepreneurial ventures and start-ups. The management of tertiary institutions were recommended to positively influence employees to engage in retirement savings by funding employees to attend financial literacy and investment management training such that they would acquire the necessary knowledge to make savings and investments for post-retirement. Furthermore, institutions were recommended to hold quarterly and semi-annual seminars and conferences on retirement planning and retirement savings and make attendance by employees’ mandatory such that their attitude on retirement savings increases. VL - 1 IS - 1 ER -

Commerce Division, Harare Polytechnic, Harare, Zimbabwe

Faculty of Business Management Sciences and Economics, University of Zimbabwe, Harare, Zimbabwe

Faculty of Business Management Sciences and Economics, University of Zimbabwe, Harare, Zimbabwe

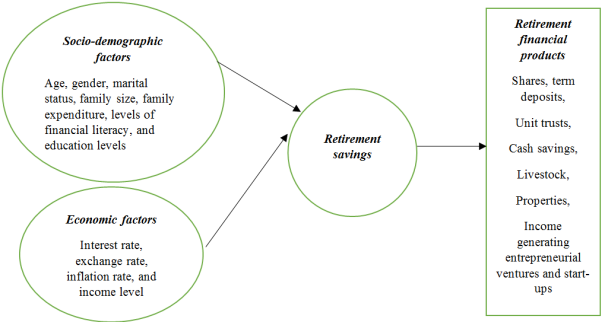

Figure 1. The Conceptual framework, Source: Primary data (2025).

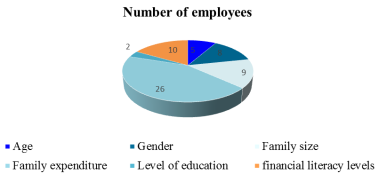

Figure 2. The socio-demographic determinants which influence retirement savings of employees in tertiary institutions of Zimbabwe, Source: primary data, (2025).

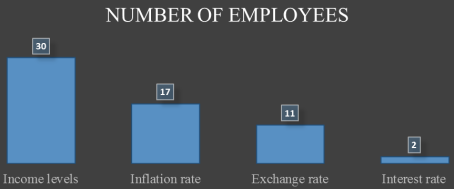

Figure 3. The economic factors which influence retirement savings of employees in tertiary institutions of Zimbabwe, Source: primary data, (2025).